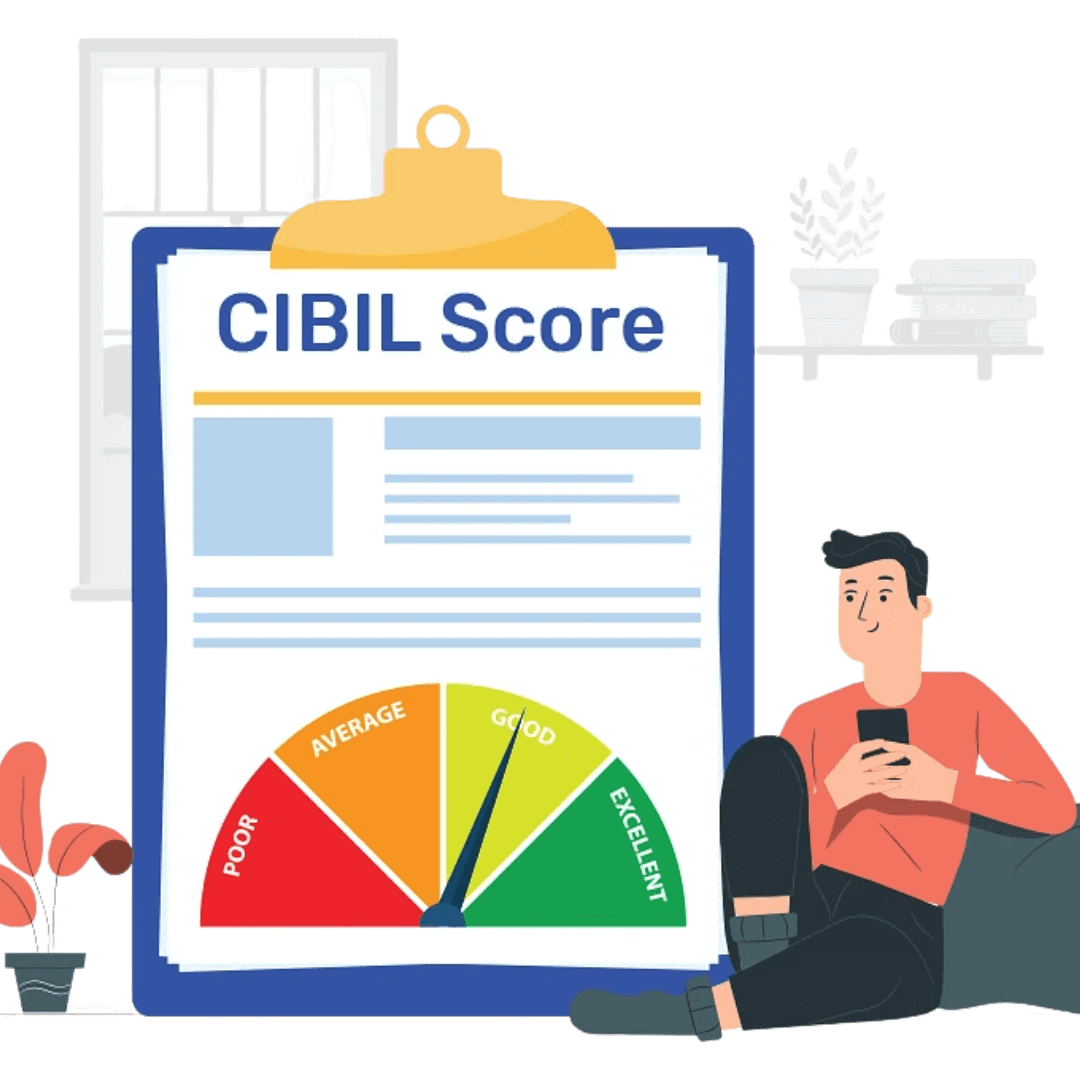

CIBIL SCORE

Credit Score

A Credit Score, also commonly referred to as CIBIL Score, is a 3-digit number that represents how well you have managed credit, like a home loan or personal loan or your credit cards, in the past. It is primarily a measure of your ability to borrow – calculated basis your past behaviour with credit.

Simply put, your credit score shows lenders whether you are a reliable borrower or a risky one, and the likelihood of you repaying a new loan responsibly.

When you apply for any kind of loan or a credit card, the lender bank or NBFC takes a close look at your credit score and credit history that is maintained in your credit report. Your credit score is calculated out of 900. The higher your credit score, the more likely lenders are to approve you for new credit. Usually, a score of 750 and above is preferred by lenders.

CIBIL or Credit Information Bureau (India) Limited is a credit bureau that maintains and calculates your credit score. While CIBIL is the oldest, there are three other credit bureaus that provide you with your credit report – Experian, CRIF High Mark and Equifax. Each credit bureau calculates your credit score independently on the basis of your credit information that is provided to them by banks and NBFCs on a regular basis. Each credit bureau has its own model for calculating your credit score; hence, your score from each bureau is likely to vary.

In stock

₹4,999 ₹9,999

Credit Score

A Credit Score, also commonly referred to as CIBIL Score, is a 3-digit number that represents how well you have managed credit, like a home loan or personal loan or your credit cards, in the past. It is primarily a measure of your ability to borrow – calculated basis your past behaviour with credit.

Simply put, your credit score shows lenders whether you are a reliable borrower or a risky one, and the likelihood of you repaying a new loan responsibly.

When you apply for any kind of loan or a credit card, the lender bank or NBFC takes a close look at your credit score and credit history that is maintained in your credit report. Your credit score is calculated out of 900. The higher your credit score, the more likely lenders are to approve you for new credit. Usually, a score of 750 and above is preferred by lenders.

CIBIL or Credit Information Bureau (India) Limited is a credit bureau that maintains and calculates your credit score. While CIBIL is the oldest, there are three other credit bureaus that provide you with your credit report – Experian, CRIF High Mark and Equifax. Each credit bureau calculates your credit score independently on the basis of your credit information that is provided to them by banks and NBFCs on a regular basis. Each credit bureau has its own model for calculating your credit score; hence, your score from each bureau is likely to vary.

Why Credit Score is Very Important

Your credit score is the first thing that a lender looks at while evaluating your loan application. In case your CIBIL score or credit score is low, the lender might reject the application without even considering it further.

If the score is high, the lender will look into other details to determine if the applicant is creditworthy. Thus, a good credit score increases the chances of your loan application being approved.

However, your credit score is not the only factor considered for a person’s ability to secure new credit. Lenders also take into consideration your debt to income ratio, employment history, profession, etc. before approving/rejecting the application.

How is your Credit Score calculated?

Your credit score depends on a lot of factors that a credit bureau takes into consideration while calculating your score. These factors depict your credit behaviour in the past and are reported to Banks and NBFCs every time you apply for a credit product. Some of the key factors that influence your credit score are:

Loan Repayment History: Timely payments can boost up your credit score and help in improving it significantly. Defaulting on your EMIs or making late payments negatively affects your credit score. Your loan repayment history has a high impact on your CIBIL score calculation.

Duration of Credit History: The duration or age of your credit history also affects your credit score. If you have used credit cards/loans for a long period of time and made timely payments on them, then it’s a sign of disciplined credit behaviour. It has a medium impact on your credit score.

Number of Hard Inquiries: Every time you apply for a new credit product, the lender makes an inquiry about your credit score. Such inquiries by lenders and financial institutions are known as hard inquiries. Too many hard inquiries may negatively affect your credit score as it shows you to be credit hungry. Multiple hard enquiries at the same time may have a considerable short-term impact on your credit score.

Credit Utilization Ratio: The ratio of the credit amount you spend to the credit amount available to you is known as the credit utilization ratio. You should try to refrain from utilising more than 30% of your available credit on a regular basis to have a good credit utilization ratio. Even though having CUR in the range of 60-70% barely has an impact on your credit score but having a high credit utilization ratio or maxing out your credit limit frequently indicates a higher dependency on credit and a potentially high repayment burden, which may negatively impact your credit score.

Credit Mix: If you have taken different kinds of loans like personal loan, auto loan, home loan and have responsibly paid it back, it shows your ability to handle different kinds of credit. Also, if you have taken too many unsecured loans like personal loans, it shows you are credit hungry and are too dependent on credit. This may work against you. However, credit mix has a low impact on your credit score and it’s unlikely that a lender will reject you just because you do not have an optimum mix of credit products.

Other Factors: Apart from the above 5 factors, which are primary in calculating your CIBIL score, there are other factors like errors in your credit report, lack of credit history and inability to fulfil your role as loan guarantor may have a very low negative impact on your credit score.

What is considered a good credit score?

After the pandemic, most lenders have raised the eligibility criteria for approving a loan. Today, most lenders consider a credit score of 760 and above from CIBIL or any credit bureau as an excellent credit score. It becomes relatively easier to get the loan or credit card application approved if you have a CIBIL score of 760+.

Every credit bureau uses its own formula to calculate your credit score. Thus, your score may vary from one credit bureau to another.

It is possible to have a CIBIL score of 760 or above and have a credit score from another bureau below 700 at the same time. Hence, it’s important that you keep a tab on credit score from multiple bureaus. It is advisable to check your credit score once every 3-4 months at least.

Let us have a look at the credit score range that most lenders and bureaus consider while evaluating your credit applications:

| Above 800 | Excellent |

| 761-800 | Good |

| 701-760 | Fair |

| 601-700 | Low |

| 300-600 | Very Low |

Please Note: The credit score range mentioned above is only indicative and may vary from lender to lender and from one bureau to another.

Benefits of maintaining a High Credit Score

Though credit score is not the only thing that lenders look at when considering a loan or credit card application, it is arguably one of the most important ones. Maintaining a good credit score comes with several benefits that include:

- Greater chances of your loan applications being approved, as a high credit score indicates higher creditworthiness and lower risk for the lender

- You are more likely to receive lower interest rates on loans

- You can get easy and quick approval for your loan and credit card applications

- Access to pre-approved loans based on your eligibility

- You can avail higher limit on your credit cards

- Discount on processing fees and other charge

Why is your credit score low?

There can be a number of reasons for a low credit score. Some of the main factors that can lower your credit score are:

- Missed or late payments of credit cards and loan EMIs

- Maxing out your credit limit or having very high credit utilization ratio regularly

- Errors in your credit report can also lower your score significantly

- Frequent or multiple hard inquiries for credit can also damage your credit score

- Closing the oldest credit account if other credit accounts are relatively new (It reduces the age of credit history)

- Settling the loan or credit card account instead of paying it in full and closing the account.

What to do if your credit score is low?

A low credit score can make it difficult for you to get your loan or credit card applications approved. You can take the following steps and adhere strictly to it to improve your credit score again:

- Start paying your loan EMIs and credit card bills on time. Do not miss payments under any circumstances.

- Reduce your excessive dependency on credit and keep your credit utilization ratio below 30% regularly.

- In case of errors in your credit report, get it rectified at the earliest from the credit bureau. For this, you should check your credit score regularly through Many Platforms and if there’s a fall, do check the report for errors.

- Avoid applying for multiple loans or credit cards very frequently. It is advisable to wait for six months from availing the latest credit instrument before you apply for credit again.

- Avoid closing your oldest credit card. A longer credit history helps lenders take credit-related decisions with more confidence.

- Keep a good mix of secured (eg. home loan, car loan, etc.) and unsecured credit (personal loan, credit card, etc.) in your profile.

- Seek expert advice from our Credit Advisory Services to improve your credit score significantly.

Credit Report includes the following key information:

- Name

- Date of birth

- Permanent Account Number(PAN)

- Aadhar Card

- Additional Identity Information such as the serial number of Driving License, Voter’s ID card, etc.

- Current and previous residential addresses

- Current and previous employers with their address

- Income tax information availed through previous IT filings

- Dates on which your credit report was pulled by lenders to determine loan/credit card eligibility

- Information related to overdraft facilities available with your banking accounts, etc.

REQUIREMENTS FOR THE CREDIT SCORE CHECK:-

- Identity proof(any 1)

- Address proof

- Electricity bill

- Income proof

Related products

-

Bharat Inc., TDS, PF & ESI

ESI Returns Filings

Description: ESI registered businesses have to file ESI returns on monthly basis. It is governed under the ESI Act, 1948; ESIC (Employees’ State Insurance Corporation) which provides benefits to employees in the event of their sickness, death, disablement, injury, etc.

SKU: EBFWAXWM -

Bharat Inc., IPR & QUALITY

Design Registration

Design Registration

Design registration gives exclusive right to its owner and creator. The registration gives authority to the creator to use the design for a period of ten years, the time period can be extended for five more years. In case of any infringement, the owner can seek legal help under the Design Act.

SKU: EB72BFXU -

Bharat Inc., IPR & QUALITY, TAX FILINGS & COMPLIANCE

GeM Registration

GeM Registration

GeM is a short form of one stop Government e-Market Place hosted by DGS&D where common user goods and services can be procured. GeM is dynamic, self-sustaining and user friendly portal for making procurement by Government officers.

The portal was launched on 9th August 2016 by the Commerce & Industry Minister. Note: Prices Mentioned Below Are Exclusive Of Taxes.

SKU: EB61181F -

Bharat Inc., TDS, PF & ESI

TDS Returns

Description: Apart from depositing the tax the deductor also has to do TDS return filing. TDS return filing is a quarterly statement that is to be given to the Income Tax department. Once the TDS returns are submitted the details will come up on Form 26 AS.

SKU: EBKZU71G -

Bharat Inc., IPR & QUALITY, TAX FILINGS & COMPLIANCE

Udyog Aadhar Registration

Udyog Aadhar Registration

Udyog Aadhaar (also called as Aadhaar for Business) is a unique 12-digit Government identification number provided by the Ministry of MSME for the small and medium enterprises to register themselves as MSME.

Unlike other business entities, a sole proprietor business owner does not have an official recognition of his business. Udyog Aadhaar is highly advisable for Sole Proprietors who dont have an official govt recognition as udyog aadhaar helps a sole proprietor get a unique identity and official registration with the Government of India that validates the existence of his business.

Other types of business entities usually have a official recognition and they can register for Udyog Aadhaar and avail the other benefits offered by MSME as mentioned below

SKU: EBA9BVQP